...

Contains many important findings. here are just two

1. New estimates of labour productivity suggest that changes in the

aggregate mix of activity in the UK economy – as well as lower

productivity growth in telecommunications, manufacturing and finance

industries – account for a large proportion of the UK’s recent

productivity slowdown.

2. Experimental estimates indicate that current price investment in

intangible assets was £134.2 billion in 2015, compared with £141.7

billion for investment in tangible assets over the same period; this is

the first time since 2000 that investment in tangible assets has been

higher than investment in intangible assets

In turn.

1. Industries and industry mix.

in this release we have extended the time series of our detailed-industry labour productivity dataset back to 1997.

These data include labour productivity data for 66 different industry

groupings and for around 50 “division” level industries from the

Standard Industrial Classification 2007: SIC 2007

There's a lot of within industry heterogeneity

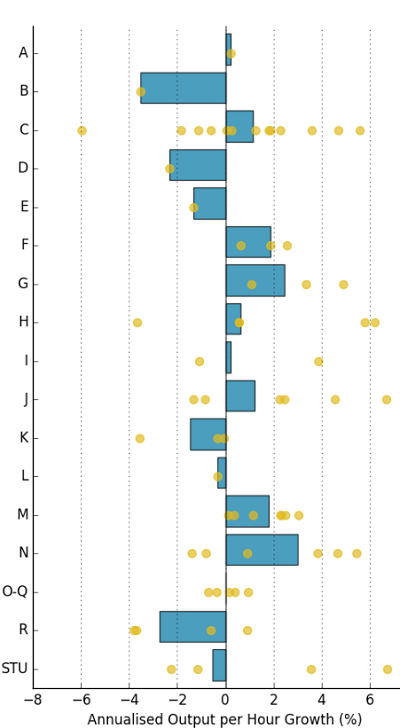

Figure 1 shows the annualised compound average growth rates of labour

productivity between Quarter 1 (Jan to Mar) 2009 and Quarter 1 2017, for

both industry sections (an aggregated industry breakdown – the bars),

and the lower, division-level components of those industries (the

points)

A: Agriculture, forestry and fishing; B: Mining and quarrying; C:

Manufacturing; D: Electricity, gas, steam and air conditioning supply;

E: Water supply, sewerage, waste management and remediation activities;

F: Construction; G: Wholesale and retail trade; repair of motor vehicles

and motorcycles; H: Transportation and storage; I: Accommodation and

food service activities; J: Information and communication; K: Financial

and insurance activities; L: Real estate activities; M: Professional,

scientific and technical activities; N: Administrative and support

service activities; O-Q: Public administration, defence, education,

human health and social work activities; R: Arts, entertainment and

recreation; and STU: Other service activities; activities of household

and extra-territorial organisations and bodies.

Which industry is the largest contributor? This is interesting:

growth in whole economy labour productivity can be decomposed into

contributions from each industry – reflecting the effect that

productivity growth within an industry has on the UK’s aggregate

performance – as well as an allocation effect. This allocation effect

captures changes in the mix of different industries in the UK economy

overall, in terms of both shares in value added and shares of labour

input. For instance, if the share of labour input used by a

low-productivity (high-productivity) industry increases through time at

the expense of high-productivity (low-productivity) industries, then the

UK’s aggregate performance will weaken (strengthen), independent of the

growth rates of productivity within specific industries. In other

words, productivity in each individual industry could increase, but

overall productivity could still fall if sufficient labour moved from

higher to lower productivity industries.

By comparing the contributions to labour productivity growth of specific

industries prior to the downturn with the equivalent contributions to

growth following the downturn, the change in contributions can be used

to help explain the slowdown of whole economy productivity growth. This

is shown in Figure 2, which uses the new, longer time series of labour

productivity to compare contributions to growth in the five years to

Quarter 3 (July to Sept) 2007 (the light points) with contributions to

growth in the five years to Quarter 3 2017 (the dark points). The

differences between these points are shown as bars and these represent

the change in the contribution of each industry to aggregate labour

productivity growth over this period. Industries are ordered from those

whose contribution increased the most, to those whose contribution was

most reduced. The same is also done for the allocation effect. To

highlight the important results, only the top 10 and bottom 10

contributors are shown

Notes: 68: Real estate activities; B: Mining and quarrying; 85: Education; 60:

Programming and broadcasting activities; 45: Wholesale and retail trade

and repair of motor vehicles and motorcycles; 41: Construction of

buildings; 43: Specialised construction activities; 46: Wholesale trade,

except of motor vehicles and motorcycles; 84: Public administration and

defence; compulsory social security; 59: Motion picture, video and

television programme production, sound recording and music publishing

activities; 56: Food and beverage service activities; 71: Architectural

and engineering activities; technical testing and analysis; CK:

Manufacture of machinery and equipment n.e.c.; CF: Manufacture of basic

pharmaceutical products and pharmaceutical preparations; 78: Employment

activities; 66: Activities auxiliary to financial services and insurance

activities; CH: Manufacture of basic metals and metal products; 61:

Telecommunications; and 64: Financial service activities, except

insurance and pension funding.

So it turns out that reallocation is the biggest contributor.

Firstly, at this level of detail1, the allocation effect

accounts for 5 percentage points of the 7.1 percentage points slowdown

in productivity between the two periods. This means that changes in the

mix of industries in which individuals are employed accounts for the

largest proportion of the slowdown in growth in recent years. Rather

than adding to labour productivity growth as it did over the five years

to Quarter 3 2007, the allocation effect held back output per hour

growth over this period.

Secondly, the slowdown in measured productivity

growth in several industries plays an important role in explaining the

slowdown in the UK’s aggregate performance in recent years. In

particular, the telecommunications2, finance, and manufacturing industries made considerable contributions over this period.

The allocation formula is hard to find, it is in this

information

note (thanks to ONS for providing this).

And says that the reallocation effect is the sum of (a) the movement of labour to above- or below-average industries and (b) the covariance between productivity growth and labour share growth. Notice that the allocation effect was positive before the great recession and negative afterwards.

more details on this are found here. My reading is that there has been a collapse in the labour effect, that is, much of the reallocation problem seems to be a a fall in the extent to which labour is flowing to high productivity industries.

This below diagram is figure 9 from https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/divisionlevellabourproductivityestimates/january2018#the-effect-of-reallocation-on-output-per-hour-growth.

This below diagram is figure 9 from https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/divisionlevellabourproductivityestimates/january2018#the-effect-of-reallocation-on-output-per-hour-growth.